Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)

kst_roc4 = ta.roc(close, 30)

kst = ta.sma(kst_roc1, 10) + 2*ta.sma(kst_roc2, 10) + 3*ta.sma(kst_roc3, 10) + 4*ta.sma(kst_roc4, 15)

// 51. Percentage Price Oscillator (PPO)

ppo_line = ((ta.ema(close, 12) - ta.ema(close, 26)) / ta.ema(close, 26)) * 100

ppo_signal = ta.ema(ppo_line, 9)

ppo_histogram = ppo_line - ppo_signal

// |----- PLOT MAIN INDICATORS -----| //

// Plot key momentum indicators

plot(rsi_centered, title="01_RSI_Centered", color=color.purple, linewidth=1)

plot(stoch_centered, title="02_Stoch_Centered", color=color.blue, linewidth=1)

plot(williams_r, title="03_Williams_R", color=color.red, linewidth=1)

plot(macd_histogram, title="04_MACD_Histogram", color=color.orange, linewidth=1)

plot(cci, title="05_CCI", color=color.green, linewidth=1)

// Plot trend indicators

plot(sma_momentum, title="06_SMA_Momentum", color=color.navy, linewidth=1)

plot(ema_momentum, title="07_EMA_Momentum", color=color.maroon, linewidth=1)

plot(sar_trend, title="08_SAR_Trend", color=color.teal, linewidth=1)

plot(lr_slope, title="09_LR_Slope", color=color.lime, linewidth=1)

plot(mac, title="10_MAC", color=color.fuchsia, linewidth=1)

// Plot volatility indicators

plot(atr_pct, title="11_ATR_Pct", color=color.yellow, linewidth=1)

plot(bb_position, title="12_BB_Position", color=color.aqua, linewidth=1)

plot(kc_position, title="13_KC_Position", color=color.olive, linewidth=1)

plot(std_dev_pct, title="14_StdDev_Pct", color=color.silver, linewidth=1)

plot(bb_width, title="15_BB_Width", color=color.gray, linewidth=1)

// Plot volume indicators

plot(vroc, title="16_VROC", color=color.blue, linewidth=1)

plot(eom_sma, title="17_EOM", color=color.red, linewidth=1)

plot(vol_osc, title="18_Vol_Osc", color=color.green, linewidth=1)

plot(force_index_sma, title="19_Force_Index", color=color.orange, linewidth=1)

plot(obv, title="20_OBV", color=color.purple, linewidth=1)

// Plot additional oscillators

plot(ao, title="21_Awesome_Osc", color=color.navy, linewidth=1)

plot(cmo, title="22_CMO", color=color.maroon, linewidth=1)

plot(dpo, title="23_DPO", color=color.teal, linewidth=1)

plot(trix, title="24_TRIX", color=color.lime, linewidth=1)

plot(fisher, title="25_Fisher", color=color.fuchsia, linewidth=1)

// Plot more momentum indicators

plot(mfi_centered, title="26_MFI_Centered", color=color.yellow, linewidth=1)

plot(ac, title="27_AC", color=color.aqua, linewidth=1)

plot(ppo_pct, title="28_PPO_Pct", color=color.olive, linewidth=1)

plot(stoch_rsi_centered, title="29_StochRSI_Centered", color=color.silver, linewidth=1)

plot(klinger, title="30_Klinger", color=color.gray, linewidth=1)

// Plot trend continuation

plot(tii, title="31_TII", color=color.blue, linewidth=1)

plot(ichimoku_signal, title="32_Ichimoku_Signal", color=color.red, linewidth=1)

plot(mama_momentum, title="33_MAMA_Momentum", color=color.green, linewidth=1)

plot(zlema_momentum, title="34_ZLEMA_Momentum", color=color.orange, linewidth=1)

plot(bop, title="35_BOP", color=color.purple, linewidth=1)

// Plot volume continuation

plot(nvi, title="36_NVI", color=color.navy, linewidth=1)

plot(pvi, title="37_PVI", color=color.maroon, linewidth=1)

plot(momentum_pct, title="38_Momentum_Pct", color=color.teal, linewidth=1)

plot(roc, title="39_ROC", color=color.lime, linewidth=1)

plot(rvi, title="40_RVI", color=color.fuchsia, linewidth=1)

// Plot volatility continuation

plot(dc_position, title="41_DC_Position", color=color.yellow, linewidth=1)

plot(rvi_volatility, title="42_RVI_Volatility", color=color.aqua, linewidth=1)

plot(hv, title="43_Historical_Vol", color=color.olive, linewidth=1)

plot(gk_volatility, title="44_GK_Volatility", color=color.silver, linewidth=1)

plot(parkinson, title="45_Parkinson_Vol", color=color.gray, linewidth=1)

// Plot final oscillators

plot(rogers_satchell, title="46_RS_Volatility", color=color.blue, linewidth=1)

plot(elder_power, title="47_Elder_Power", color=color.red, linewidth=1)

plot(stc, title="48_STC", color=color.green, linewidth=1)

plot(coppock, title="49_Coppock", color=color.orange, linewidth=1)

plot(kst, title="50_KST", color=color.purple, linewidth=1)

// Plot final indicators

plot(ppo_histogram, title="51_PPO_Histogram", color=color.navy, linewidth=1)

plot(pvt, title="52_PVT", color=color.maroon, linewidth=1)

// |----- Reference Lines -----| //

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dashed, linewidth=1)

hline(50, "Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-50, "Lower Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(25, "Upper Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-25, "Lower Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

// |----- Enhanced Information Table -----| //

if show_table and barstate.islast

table_position = position.top_right

table_text_size = table_size == "Tiny" ? size.tiny : table_size == "Small" ? size.small : size.normal

var table info_table = table.new(table_position, 3, 18, bgcolor=color.new(color.white, 85), border_width=1, border_color=color.gray)

// Headers

table.cell(info_table, 0, 0, 'Category', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 1, 0, 'Indicator', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 2, 0, 'Value', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

// Key Momentum Indicators

table.cell(info_table, 0, 1, 'MOMENTUM', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 1, 'RSI Centered', text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 2, 1, str.tostring(rsi_centered, '0.00'), text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 0, 2, '', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 1, 2, 'Stoch Centered', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 2, str.tostring(stoch_centered, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 3, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 3, 'Williams %R', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 3, str.tostring(williams_r, '0.00'), text_color=color.red, text_size=table_text_size)

table.cell(info_table, 0, 4, '', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 1, 4, 'MACD Histogram', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 2, 4, str.tostring(macd_histogram, '0.000'), text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 0, 5, '', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 1, 5, 'CCI', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 2, 5, str.tostring(cci, '0.00'), text_color=color.green, text_size=table_text_size)

// Key Trend Indicators

table.cell(info_table, 0, 6, 'TREND', text_color=color.navy, text_size=table_text_size, bgcolor=color.new(color.navy, 90))

table.cell(info_table, 1, 6, 'SMA Momentum %', text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 2, 6, str.tostring(sma_momentum, '0.00'), text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 0, 7, '', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 1, 7, 'EMA Momentum %', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 2, 7, str.tostring(ema_momentum, '0.00'), text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 0, 8, '', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 1, 8, 'SAR Trend', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 2, 8, str.tostring(sar_trend, '0'), text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 0, 9, '', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 1, 9, 'Linear Regression', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 2, 9, str.tostring(lr_slope, '0.000'), text_color=color.lime, text_size=table_text_size)

// Key Volatility Indicators

table.cell(info_table, 0, 10, 'VOLATILITY', text_color=color.yellow, text_size=table_text_size, bgcolor=color.new(color.yellow, 90))

table.cell(info_table, 1, 10, 'ATR %', text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 2, 10, str.tostring(atr_pct, '0.00'), text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 0, 11, '', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 1, 11, 'BB Position', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 2, 11, str.tostring(bb_position, '0.00'), text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 0, 12, '', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 1, 12, 'KC Position', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 2, 12, str.tostring(kc_position, '0.00'), text_color=color.olive, text_size=table_text_size)

// Key Volume Indicators

table.cell(info_table, 0, 13, 'VOLUME', text_color=color.blue, text_size=table_text_size, bgcolor=color.new(color.blue, 90))

table.cell(info_table, 1, 13, 'Volume ROC', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 13, str.tostring(vroc, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 14, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 14, 'EOM', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 14, str.tostring(eom_sma, '0.000'), text_color=color.red, text_size=table_text_size)

// Key Oscillators

table.cell(info_table, 0, 15, 'OSCILLATORS', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 15, 'Awesome Osc', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 15, str.tostring(ao, '0.000'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 16, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 16, 'Fisher Transform', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 16, str.tostring(fisher, '0.000'), text_color=color.red, text_size=table_text_size)

// Summary Statistics

table.cell(info_table, 0, 17, 'SUMMARY', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.gray, 70))

table.cell(info_table, 1, 17, 'Total Indicators: 52', text_color=color.black, text_size=table_text_size)

regime_color = rsi_centered > 10 ? color.green : rsi_centered < -10 ? color.red : color.gray

regime_text = rsi_centered > 10 ? "BULLISH" : rsi_centered < -10 ? "BEARISH" : "NEUTRAL"

table.cell(info_table, 2, 17, regime_text, text_color=regime_color, text_size=table_text_size)

This makes it the perfect “indicator backbone” for quantitative and systematic traders who want to prototype, combine, and test new regime detection models—especially in combination with the Markov Chain indicator.

How to use this script with the Markov Chain for research and backtesting:

Add the Enhanced Indicator Export to your chart.

Every calculated indicator is available as an individual data stream.

Connect the indicator(s) you want as custom input(s) to the Markov Chain’s “Custom Indicators” option.

In the Markov Chain indicator’s settings, turn ON the custom indicator mode.

For each of the three custom indicator inputs, select the exported plot from the Enhanced Export script—the menu lists all 45+ signals by name.

This creates a powerful, modular regime-detection engine where you can mix-and-match momentum, trend, volume, or custom combinations for advanced filtering.

Backtest regime logic directly.

Once you’ve connected your chosen indicators, the Markov Chain script performs regime detection (Bull/Neutral/Bear) based on your selected features—not just price returns.

The regime detection is robust, automatically normalized (using Z-score), and outputs bias (1, -1, 0) for plug-and-play integration.

Export the regime bias for programmatic use.

As described above, use input.source() in your Pine Script strategy or system and link the bias output.

You can now filter signals, control trade direction/size, or design pairs-trading that respect true, indicator-driven market regimes.

With this framework, you’re not limited to static or simplistic regime filters. You can rigorously define, test, and refine what “market regime” means for your strategies—using the technical features that matter most to you.

Optimize your signal generation by backtesting across a universe of meaningful indicator blends.

Enhance risk management with objective, real-time regime boundaries.

Accelerate your research: iterate quickly, swap indicator components, and see results with minimal code changes.

Automate multi-asset or pairs-trading by integrating regime context directly into strategy logic.

Add both scripts to your chart, connect your preferred features, and start investigating your best regime-based trades—entirely within the TradingView ecosystem.

References & Further Reading

Ang, A., & Bekaert, G. (2002). “Regime Switches in Interest Rates.” Journal of Business & Economic Statistics, 20(2), 163–182.

Hamilton, J. D. (1989). “A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle.” Econometrica, 57(2), 357–384.

Markov, A. A. (1906). "Extension of the Limit Theorems of Probability Theory to a Sum of Variables Connected in a Chain." The Notes of the Imperial Academy of Sciences of St. Petersburg.

Guidolin, M., & Timmermann, A. (2007). “Asset Allocation under Multivariate Regime Switching.” Journal of Economic Dynamics and Control, 31(11), 3503–3544.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets. New York Institute of Finance.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns.” Journal of Finance, 47(5), 1731–1764.

Zucchini, W., MacDonald, I. L., & Langrock, R. (2017). Hidden Markov Models for Time Series: An Introduction Using R (2nd ed.). Chapman and Hall/CRC.

On Quantitative Finance and Markov Models:

Lo, A. W., & Hasanhodzic, J. (2009). The Heretics of Finance: Conversations with Leading Practitioners of Technical Analysis. Bloomberg Press.

Patterson, S. (2016). The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution. Penguin Press.

TradingView Pine Script Documentation: www.tradingview.com

TradingView Blog: “Use an Input From Another Indicator With Your Strategy” www.tradingview.com

GeeksforGeeks: “What is the Difference Between Markov Chains and Hidden Markov Models?” www.geeksforgeeks.org

What makes this indicator original and unique?

- On‑chart, real‑time Markov. The chain is drawn directly on your chart. You see the current regime, its tendency to stay (self‑loop), and the usual next step (arrows) as bars confirm.

- Source‑agnostic by design. The engine runs on any series you select via input.source() — price, your own oscillator, a composite score, anything you compute in the script.

- Automatic normalization + regime mapping. Different inputs live on different scales. The script standardizes your chosen source and maps it into clear regimes (e.g., Bull / Bear / Neutral) without you micromanaging thresholds each time.

- Rolling, bar‑by‑bar learning. Transition tendencies are computed from a rolling window of confirmed bars. What you see is exactly what the market did in that window.

- Fast experimentation. Switch the source, adjust the window, and the Markov view updates instantly. It’s a rapid way to test ideas and feel regime persistence/switch behavior.

Integrate your own signals (using input.source())

- In settings, choose the Source . This is powered by input.source() .

- Feed it price, an indicator you compute inside the script, or a custom composite series.

- The script will automatically normalize that series and process it through the Markov engine, mapping it to regimes and updating the on‑chart spheres/arrows in real time.

Credits:

Deep gratitude to @RicardoSantos for both the foundational Markov chain processing engine and inspiring open-source contributions, which made advanced probabilistic market modeling accessible to the TradingView community.

Special thanks to @Alien_Algorithms for the innovative and visually stunning 3D sphere logic that powers the indicator’s animated, regime-based visualization.

Disclaimer

This tool summarizes recent behavior. It is not financial advice and not a guarantee of future results.

Pesquisar nos scripts por "high low"

ICT Smart Money Trading Suite [SwissAlgo]ICT/Smart Money Trading Suite - Technical Analysis Indicator

----------------------------------------------------------

OVERVIEW

The ICT/Smart Money Trading Suite is a technical analysis indicator that implements concepts from Inner Circle Trader (ICT) methodology and Smart Money Concepts (SMC).

ICT methodology was developed by Michael J. Huddleston (ICT) and focuses on understanding Institutional market behavior.

Smart Money Concepts builds upon these ideas to analyze how large Financial Institutions and/or Market Makers seem to operate in the markets.

This indicator combines multiple analytical tools into a single package for market structure analysis, imbalance detection, and the observation of institutional order flow.

----------------------------------------------------------

CORE COMPONENTS

Market Structure Analysis:

- External Structure : Major swing highs and lows that define broader price movement (these are the most significant structural points that institutions reference for their positioning and typically require substantial volume and momentum to break)

- Internal Structure : Shorter-term pivots showing micro-trend developments within the External Structure (these internal pivot highs and lows often represent areas where retail traders may be positioned on the wrong side of the market as they frequently form just before major structural breaks or trend continuations, creating liquidity that institutions can utilize)

- Structural Breakout Detection : Identification of structure breaks and potential trend changes ( 'Change of Character' which occurs when the External Structure shifts from bullish to bearish bias or vice-versa indicating a potential major trend reversal, and 'Break of Structure' which happens when price decisively takes out previous significant highs in a bearish trend or previous significant lows in a bullish trend confirming trend continuation or acceleration)

- EMA Cloud : Dynamic support and resistance zones with trend context (additional reference point)

Imbalance Zone Detection:

Fair Value Gaps (FVGs):

Price inefficiencies that occur between candles when sudden price moves create gaps in price delivery

Typically formed when the low of a bullish candle is higher than the high of the candle two periods prior, or when the high of a bearish candle is lower than the low of the candle two periods prior

These gaps represent areas where price moved too quickly without adequate two-way auction process

Institutions may return to fill these inefficiencies at a later time for proper price discovery

The theory suggests that all price ranges should eventually be traded through to complete the auction process

Gaps are automatically removed from the chart when price fully retraces back through the inefficient area

Order Blocks (OBs):

Specific candles that occur immediately before significant market moves and represent institutional decision points

Identified as the last opposing candle before a strong directional move (final bearish candle before major bullish move or final bullish candle before major bearish move)

These candles contain the orders and liquidity that institutions used as a foundation for their market manipulation

Represent areas where large institutional players positioned themselves to move the market significantly

Price may return to these levels to collect additional liquidity or test institutional resolve

The candle's full range (high to low) is considered the active zone where institutional interest may remain

Vector Candle Recovery:

Zones created by high-activity candles that demonstrate unusually large range and volume characteristics

These candles are interpreted as manipulative price pushes designed to hunt liquidity and trigger stop losses

Often used by institutions to induce retail traders into poor positions before reversing direction

Recovery zones represent the full range of these vector candles where price may retrace

The concept assumes that extreme moves often get partially retraced as the market corrects from artificial price displacement

Zones are invalidated when a significant portion of the vector candle range is retraced (typically 50% or more)

Support & Resistance:

Key price zones based on historical price reactions and pivot clustering analysis

Calculated through algorithmic identification of areas where price has repeatedly found buyers (support) or sellers (resistance)

Strength is determined by the number of times price has reacted from these levels and the volume of activity at these zones

Represent psychological and algorithmic reference points where institutional systems are likely to place orders

Create areas of increased probability for price reactions due to concentration of pending orders and decision-making activity

Zones are color-coded based on current price position: green for support (price above), red for resistance (price below), yellow for neutral (price within)

Liquidity Analysis:

- Liquidity Pools : Areas above or below key levels where stop orders may cluster

- Kill Zones : Time-based periods associated with increased market activity

- Daily/Weekly/Monthly Price Levels : Key institutional reference points (price highs/lows)

Vector Candles/Price Manipulation:

Advanced algorithm identifying statistically significant candles using volume delta analysis, range statistics, and persistence scoring.

----------------------------------------------------------

VISUAL INTERPRETATION - DETAILED GUIDE

MARKET STRUCTURE

External Structure (Thick Lines):

- Green thick lines: Major support levels (external lows) that define bullish structure

- Red thick lines: Major resistance levels (external highs) that define bearish structure

- These lines represent significant swing points that institutions may reference

- Lines extend from the swing point and update as the structure evolves

Internal Structure (Thin Lines):

- Green thin lines: Minor support levels showing internal market structure

- Red thin lines: Minor resistance levels showing internal market structure

- More frequent updates than external structure, showing micro-trend changes

Structure Markers:

- Small triangles with "H": External pivot highs (major resistance points)

- Small triangles with "L": External pivot lows (major support points)

- Small dots: Internal pivot points (minor structure without text)

- Markers appear with a 20-bar delay to confirm pivot validity

HIGHS/LOWS LEVELS

Daily Levels (Green Dashed Lines):

- Horizontal dashed lines marking the previous day's high and low

- Updates at the start of each new trading day

- Gradient effect shows historical importance (newer = more opaque)

- Acts as institutional reference points for intraday trading

Weekly Levels (White Dashed Lines):

- Horizontal dashed lines marking the previous week's high and low

- Updates at the start of each new trading week

- Typically more significant than daily levels for swing trading

- Often respected by institutional algorithms

Monthly Levels (Orange Dashed Lines):

- Horizontal dashed lines marking the previous month's high and low

- Updates at the start of each new trading month

- Highest significance levels for long-term institutional positioning

- Major psychological and algorithmic reference points

VECTOR CANDLES

Candle Body Coloring System:

- Lime Green Bodies: Ultra-bullish vector candles (Z-score ≥ 3.0)

- Blue Bodies: Abnormal bullish vector candles (Z-score 2.0-2.99)

- Bright Red Bodies: Ultra-bearish vector candles (Z-score ≥ 3.0)

- Purple Bodies: Abnormal bearish vector candles (Z-score 2.0-2.99)

- Faded Green/Red: Normal market activity candles

Vector Identification Criteria:

- Statistical significance based on range and volume delta

- Persistence scoring (how much directional pressure remained)

- ATR-based absolute detection (candles >2x ATR automatically qualify)

- These candles often precede significant market moves or reversals

EMA CLOUD

Purple Cloud Visualization:

- Central line: 50-period EMA (blue line)

- Upper boundary: EMA + dynamic standard deviation band

- Lower boundary: EMA - dynamic standard deviation band

- Cloud fill: Purple semi-transparent area between boundaries

Interpretation:

- Price above cloud: Bullish bias context

- Price below cloud: Bearish bias context

- Price within cloud: Neutral/transitional zone

- Cloud thickness adapts to market volatility automatically

KILL ZONES

Background Highlighting:

- Yellow background tint during active kill zone periods

- London Session: 08:00-11:00 (UTC+1 time)

- NY Open: 13:00-16:00 (UTC+1 time)

- NY Close: 19:00-21:00 (UTC+1 time)

- Times automatically adjust to the chart timezone

Purpose:

- Highlights periods of typically increased institutional activity

- Times when liquidity hunting and manipulation often occur

- Periods when significant directional moves frequently begin

IMBALANCE ZONES - DETAILED BREAKDOWN

Fair Value Gaps (FVGs):

- Green boxes: Bullish FVGs (gap between bear candle high and bull candle low)

- Red boxes: Bearish FVGs (gap between bull candle high and bear candle low)

- Gray dotted lines: Midpoint of each gap (50% retracement level)

- Text label: "Fair Value Gap" in top-right corner

- Auto-removal: Boxes disappear when the price fills the gap

Order Blocks (OBs):

- Green boxes: Bullish order blocks (demand zones from the last bear candle before bullish vector)

- Red boxes: Bearish order blocks (supply zones from the last bull candle before the bearish vector)

- Gray dotted lines: Midpoint of each order block

- Text label: "OB" in top-right corner

- Invalidation: Boxes removed when price breaks below (bull OB) or above (bear OB)

Vector Candles Recovery Zones:

- Green boxes: Recovery zones after bullish vector candles

- Red boxes: Recovery zones after bearish vector candles

- Gray dotted lines: Midpoint of the vector candle range

- Text label: "Vector Recovery" on the right side

- These mark the full range of significant vector candles where retracements may occur

Support & Resistance Zones:

- Green boxes: Support zones (price currently above the zone)

- Red boxes: Resistance zones (price currently below the zone)

- Yellow boxes: Neutral zones (price within the zone)

- Text labels: "Support", "Resistance", or "Support/Resistance"

- Based on historical pivot clustering and strength analysis

Liquidity Pools:

- Green boxes: Bullish liquidity pools (below recent lows where buy stops cluster)

- Red boxes: Bearish liquidity pools (above recent highs where sell stops cluster)

- Gray dotted lines: Key liquidity level within the pool

- Text label: "Liquidity Pool" on the right side

- Zones where institutional players may hunt stop losses before reversing

----------------------------------------------------------

CALCULATION METHODOLOGY

Vector Candle Algorithm:

- Statistical Analysis using 48-bar lookback period

- Z-score thresholds: 2.0 (abnormal), 3.0 (ultra)

- ATR-based significance filtering

- Volume Delta Integration with lower timeframe analysis

- Persistence scoring based on directional pressure sustainability

- Combined scoring system (delta + range)

- Absolute Vector Detection for candles exceeding 2x ATR

Market Structure Parameters:

- Swing Size: 20-period pivot detection

- Breakout Threshold: 3 consecutive breaks for structure confirmation

- EMA Length: 50-period with dynamic cloud sizing

Fair Value Gap Detection:

- Auto Threshold: Dynamic gap sizing based on asset volatility

- Manual Threshold: User-defined minimum gap percentage

- Mitigation Logic: Automatic removal when price fills gaps

----------------------------------------------------------

TARGET USERS

This indicator is designed for traders who:

- Study Inner Circle Trader concepts

- Apply Smart Money Concepts in their analysis

- Focus on market structure and institutional behavior

- Seek confluence-based trading approaches

- Use higher timeframe bias for decision making

Experience Level: Intermediate to Advanced

Requires understanding of market structure concepts and institutional trading theory.

Recommended Timeframes:

- Analysis: 4H, Daily for market structure context

- Execution: 1H, 15min for entry timing

- Lower timeframes: With higher timeframe alignment

----------------------------------------------------------

CUSTOMIZATION OPTIONS

Display Controls:

- Master toggle for all imbalance zones

- Individual controls for each concept type

- Market structure line visibility

- Kill zone highlighting

- EMA cloud display

Visual Settings:

- Automatic light/dark mode color adaptation

- Adjustable zone transparency levels

- Extension distance controls

- Descriptive text labels

Technical Parameters:

- Vector candle sensitivity thresholds

- Historical analysis lookback periods

- Maximum zone display limits

- Zone invalidation conditions

----------------------------------------------------------

EDUCATIONAL BACKGROUND

Inner Circle Trader (ICT): A trading methodology developed by Michael J. Huddleston that focuses on understanding how institutional traders and market makers operate. The approach emphasizes market structure, liquidity concepts, and timing based on institutional behavior patterns.

Smart Money Concepts (SMC): An evolution of ICT principles that analyzes how large financial institutions move markets. These concepts include order blocks, fair value gaps, liquidity hunting, and market structure shifts.

Both methodologies are based on the premise that understanding institutional trading behavior can provide insights into market direction and timing.

----------------------------------------------------------

IMPORTANT DISCLAIMERS

This indicator is provided for educational and analytical purposes only. It is not financial advice and does not guarantee trading results.

Trading involves substantial risk of loss. Past performance does not indicate future results. Users should thoroughly understand the underlying concepts before applying them to live trading.

The effectiveness of these analytical methods may vary across different market conditions, timeframes, and instruments. Proper risk management and additional analysis are essential.

This indicator is a tool for market analysis, not a complete trading system. Success requires understanding of market principles, risk management, and continuous learning.

Always test analytical approaches thoroughly using historical data and demo accounts before implementing with real capital.

10x HTF Candles Dynamic with LTF FVG and Key LevelsPurpose

The 10x HTF Candles Dynamic Pine Script is a versatile, all-in-one trading tool designed for TradingView to empower traders with actionable insights across multiple timeframes. It combines advanced price action analysis, Fair Value Gap (FVG) detection, market structure evaluation, and key level visualization into a single, highly customizable interface. Built for day traders, swing traders, and scalpers, this script enhances decision-making by providing a clear, multi-dimensional view of market dynamics, liquidity zones, and trend biases. Its purpose is to streamline technical analysis, reduce chart clutter, and deliver real-time, visually intuitive data to support precise trading strategies.

What the Script Does

How the Script Works:

The script leverages Pine Script v5’s advanced features to deliver a robust and efficient trading tool. Below is a step-by-step explanation of its functionality:

1. Initialization and Configuration:

- Initializes with @version=5, enabling dynamic requests, and sets limits for bars (500), lines, labels, boxes, and polylines to manage resources.

- Defines user inputs for candle settings, timeframe selection, FVG parameters, DWM levels, market structure table, and visual preferences.

- Dynamically calculates 10 higher timeframes based on the current chart timeframe (e.g., 1m chart → 5m, 15m, 60m, etc.) or allows custom timeframes.

2. Data Acquisition:

- Fetches OHLC data for up to 10 timeframes using request.security, storing it in optimized TfData objects (arrays for open, high, low, close).

- Loops through enabled timeframes to minimize redundant code, improving processing speed.

3. Candlestick Rendering:

- Draws HTF candlesticks at user-defined offsets, with customizable bullish/bearish colors, wick colors, and widths.

- Calculates bar types (Inside, Normal, Outside) and optionally labels them above candles for pattern analysis.

4. FVG Detection and Visualization:

- Scans for FVGs by comparing candle highs and lows across three bars (e.g., low of candle 1 > high of candle 3 for bullish FVG).

- Detects IFVGs based on user-selected methods (wick, close, or midpoint) and highlights them with distinct colors.

- Draws FVG boxes with configurable borders, midpoint lines, and labels, tracking mitigation status.

- Limits FVG display to a user-defined maximum (1–200) to maintain chart clarity.

5. Horizontal Levels and DWM Lines:

- Computes Highs, Lows, Midpoints, and Quarter Points for each timeframe, drawing lines with customizable styles and extensions.

- Plots DWM open, close, high, low, and control point lines, with optional alerts for high/low breaks.

- Supports session-based opening price lines (e.g., 09:30 Market Open) with similar customization.

6. Market Structure and Bias:

Calculates trend bias by comparing the current close to the midpoint of the timeframe’s range (highest high to lowest low).

Updates a market structure table with timeframe, bias, and premium/discount status, using color-coded cells for quick interpretation.

7. Countdown Timers:

- Converts timeframe strings to seconds and calculates the time remaining until the next candle using timenow.

- Renders countdown labels with timeframe names (e.g., “1h\n(00:45)”) at user-defined positions.

8. Optimization and Cleanup:

- Uses VisualElements UDTs to manage lines, wicks, and labels, reducing memory usage.

- Deletes outdated drawings when limits are exceeded, ensuring a clean and responsive chart.

- Employs loops and arrays to streamline repetitive tasks, enhancing performance.

How to Use the Script:

This script is user-friendly yet powerful, suitable for traders of all experience levels. Follow these steps to maximize its potential:

1. Add to TradingView:

- Copy the script into TradingView’s Pine Editor.

- Click “Add to Chart” to apply it to your active chart.

2. Customize Settings:

- Candle Settings: Adjust the number of candles (1–10), starting position, group spacing, bullish/bearish colors, wick colors, and candle width.

- Timeframe Settings: Enable/disable up to 10 timeframes, choosing dynamic (auto-selected) or custom timeframes (e.g., 3m, 60m, D).

- FVG Settings: Toggle FVG detection, set detection methods (wick/close/midpoint), adjust thresholds, and customize colors, borders, and midpoint lines.

- DWM Settings: Enable daily/weekly/monthly lines (open, close, high, low, midpoint), set colors, and configure alerts for high/low breaks.

- Market Structure Table: Show/hide columns for timeframe, trend bias, and premium/discount, and adjust table position (top-left, bottom-right, etc.).

- Countdown Timers: Enable timers, adjust offsets, and customize text/background colors.

- Label Settings: Configure price label precision, transparency, and offsets for clarity.

3.Interpret Visuals:

- Candlesticks: Analyze HTF candles to gauge trend direction and momentum across timeframes.

- FVGs: Look for unmitigated FVGs (colored boxes) as potential support/resistance zones or trade setups.

- Key Levels: Use Highs, Lows, Midpoints, and Quarter Points to identify breakout or reversal areas.

4. Market Structure Table: Check trend bias and premium/discount status to align trades with market conditions.

- DWM Lines: Monitor daily/weekly/monthly levels for institutional reference points.

- Countdown Timers: Time entries/exits based on upcoming candle formations.

5. Integrate with Strategy:

- Combine script insights with your trading plan (e.g., use FVGs for entries, key levels for stops/targets).

- Set alerts for high/low breaks or liquidity zone approaches to stay proactive.

- Export table data or screenshot visuals for documentation and analysis.

6. Optimize Performance:

Limit the number of candles, FVGs, and lines to match your device’s capabilities.

Regularly review settings to focus on the most relevant timeframes and features.

Why the Script is Original

The 10x HTF Candles Dynamic script stands out in the TradingView community due to its innovative design, comprehensive functionality, and trader-centric approach. Here’s what makes it unique:

1. Seamless Multi-Timeframe Integration:

- Unlike single-timeframe indicators, this script synthesizes data from up to 10 timeframes, offering a holistic view of market structure.

- Dynamic timeframe selection adapts to the chart’s timeframe, ensuring relevance across all trading styles.

2 . Advanced FVG and IFVG Detection:

- Provides granular control over FVG detection with three IFVG methods (wick, close, midpoint), a rarity in most scripts.

- Tracks mitigation status and highlights unmitigated FVGs, enabling traders to capitalize on high-probability setups.

- Visualizes FVGs with boxes, midpoint lines, and labels, enhancing clarity and usability.

3. Sophisticated Market Structure Analysis:

-The bias calculation, introduced in recent updates (2 days ago), uses a robust algorithm to assess trend direction based on range midpoints.

- The market structure table, with premium/discount zones (added 20 hours ago), offers a unique summary of market conditions, unmatched by standard indicators.

4. Comprehensive DWM and Session Support:

- Integrates daily, weekly, and monthly levels alongside session-based opening prices, catering to institutional and retail traders alike.

- Customizable alerts for high/low breaks add actionable functionality.

5. Visual Hierarchy and Clarity:

- Scales line widths and transparency by timeframe, prioritizing higher timeframes for strategic focus.

- Countdown timers provide real-time context, a feature rarely seen in multi-timeframe scripts.

6.Performance Optimization:

- Recent updates introduced loops and UDTs to reduce code redundancy and boost processing speed.

- Automated cleanup mechanisms prevent chart clutter, ensuring smooth operation even on low-resource devices.

7. High Customizability:

- Offers extensive settings for visuals, timeframes, FVGs, DWM lines, and alerts, accommodating diverse trading preferences.

- Balances complexity with accessibility, making it approachable for beginners and powerful for advanced users.

8.Continuous Evolution:

- Regular updates (e.g., bias filter table, premium/discount feature, code optimization) demonstrate ongoing commitment to improvement.

- Closed-source protection (noted 20 hours ago) ensures intellectual integrity while allowing free use, fostering trust in the TradingView community.

Conclusion

The 10x HTF Candles Dynamic Pine Script is a groundbreaking tool that redefines multi-timeframe analysis on TradingView. By combining candlestick visualization, FVG detection, market structure insights, DWM levels, and countdown timers, it provides traders with a comprehensive, real-time view of market dynamics. Its advanced optimization, customization options, and continuous updates make it a standout choice for traders seeking precision, clarity, and efficiency. Whether you’re scalping intraday moves or swing trading weekly trends, this script equips you with the tools to master the markets with confidence.

[GetSparx] Lacuna Pro⚡ Lacuna Pro – Institutional Liquidity Framework

This indicator is a premium Smart Money Concepts (SMC) trading toolkit designed to help traders identify high-probability entry and exit zones by visualizing real-time market inefficiencies. It combines Fair Value Gaps (FVGs), Break of Structure (BOS), Change of Character (CHoCH), and Supply & Demand Zones into a unified, configurable framework.

Unlike many public indicators that simply "overlay concepts", this indicator implements strict internal validation to filter out noise and provide only institutional-grade levels — making it a valuable execution layer for SMC-based strategies.

🧠 What the Script Does – and Why the Combination Matters

This is more than just a combination of known SMC tools — it's a complete workflow assistant:

-FVGs highlight where liquidity is likely resting due to institutional imbalance.

-BOS & CHoCH define structural context: whether the market is trending or shifting.

-Supply & Demand Zones show where institutions are likely to react.

-Each component works together to create a layered confluence system:

-FVG inside a Demand Zone after a Bullish CHoCH → High-probability Long Setup

-Bearish BOS into a Supply Zone + fresh Bearish FVG → High-probability Short Setup

📘 Core Concepts Explained

Fair Value Gap (FVG)

FVGs occur when price moves with strong momentum and leaves a gap between candles — suggesting inefficiency. Bullish FVGs lie below price; bearish ones above. Price often returns to these levels before continuing.

An FVG is detected when a three-candle sequence reveals a price imbalance:

- Bullish : Candle 2’s low is higher than Candle 1’s high

- Bearish : Candle 2’s high is lower than Candle 1’s low

These setups indicate a sudden burst of institutional momentum, often causing price to revisit the gap for rebalancing.

Break of Structure (BOS)

A BOS signals trend continuation when price breaks the previous swing high or low in the direction of the current trend.

The script uses a 3-bar pivot system to detect local swing highs and lows — a swing high forms when the highest candle is flanked by two lower highs on each side (and vice versa for swing lows).

A BOS is confirmed when price closes beyond the most recent swing point in alignment with the current trend direction.

Change of Character (CHoCH)

A CHoCH signals a potential trend reversal by breaking a structure level in the opposite direction of the prevailing trend.

It is detected when price breaks the most recent opposing swing and simultaneously flips the internal trend state.

CHoCH events always take precedence over BOS to avoid conflicting signals.

The internal trend engine ensures that these structural shifts are valid and not caused by random volatility.

Supply & Demand Zones

These zones mark institutional interest and are formed using precise price action rules — not arbitrary support/resistance.

A valid zone begins when a small-bodied base candle (such as a star or doji) appears at a local swing point. This candle must be followed by a strong impulse candle — either a bullish engulfing (for demand) or bearish breakout (for supply).

- Demand Zone : From the base candle's low to the impulse candle's high

- Supply Zone : From the base candle's high to the impulse candle's low

These zones represent likely institutional entries or exits, often acting as magnets or rejection areas. Once price decisively breaks through a zone, it is automatically removed — keeping the chart clean and relevant.

Zone Detection Logic – When a Zone Is Drawn or Skipped

Below are the precise rules used to determine whether a Supply or Demand Zone is valid and shown on the chart

A Supply or Demand Zone is only drawn if all of the following conditions are met:

-A small-bodied base candle forms at a local high or low (body size below threshold)

-The base candle is followed by a strong impulse candle (engulfing or breakout)

-The impulse direction matches the expected context (e.g., bearish impulse from swing high = Supply)

-The candle wicks do not invalidate the structure (e.g., no long opposing wick that retraces the move)

-The zone meets the minimum size threshold based on % or ATR filter

If any of these criteria are not satisfied, the zone is skipped to avoid false or weak levels.

This ensures only clean, institutional-grade Supply & Demand Zones are shown on the chart.

(e.g. small-bodied star + bullish engulfing at swing low = Demand Zone, or bearish breakout at swing high = Supply Zone).

🔍 Core Functionality & Original Features

1. 📉 Fair Value Gaps (FVGs) – Dynamic, Validated, and Clean

Unlike scripts that draw every gap, this script applies strict quality control to ensure only meaningful FVGs appear:

Minimum Threshold Filtering

Filters out small or noisy gaps by requiring each FVG to exceed a % or ATR-based size threshold. Prevents micro-gap clutter on lower timeframes.

Momentum Candle Verification

Requires a strong middle candle (candle 2) between two extremes. Large opposing wicks invalidate the setup.

Partial Fill Adjustment

When price partially fills a gap, the FVG box automatically shrinks to show only the remaining imbalance. If fully filled, the box is removed.

Multi-Timeframe Overlays

View institutional gaps from 15m, 1H, 4H, or Daily overlaid onto any chart for top-down analysis and entry refinement.

2. 🧱 Structural Shifts – BOS & CHoCH

Structural logic is built around pivot detection with real-time trend state awareness:

Pivot Logic (Customizable Strength)

Local highs/lows are detected using pivot length (default: 3 bars left/right). Breaks are only confirmed if they align with the internal trend state.

BOS = Continuation

Breaks a swing in trend direction (e.g., HL → HH → BOS at previous HH)

CHoCH = Reversal

Breaks a structure against trend (e.g., HH → HL → break of HL = Bearish CHoCH)

Conflict Resolution

If both BOS and CHoCH could trigger, CHoCH takes priority. This avoids false positives and ensures a single, clear structure signal per swing.

Styling & Visibility

All structure lines and labels are customizable — colors, line style (solid/dashed), and which signals to display (BOS/CHoCH/both).

3. 🧠 Supply & Demand Zones – Smart Detection & Maintenance

These zones are generated using strict price action logic, not arbitrary support/resistance lines:

-Formation Conditions

-Small-bodied "base candle" at a local high/low

-Followed by an impulse candle (bullish/bearish engulfing or breakout)

-Zone Bounds

- Demand : From base candle low to impulse high

- Supply : From base candle high to impulse low

Automatic Cleanup

Once price decisively pierces a zone, it’s automatically removed from the chart. This keeps the display relevant and clutter-free.

Multi-Timeframe Zones

Toggle zones from your current timeframe or overlay from 1H, 4H, and Daily — ideal for confluence stacking.

Zone Compression Filtering

Optional compression % ensures overlapping zones are combined logically to reduce redundancy.

🧩 How It Works Together – Practical Usage Flow

This indicator is designed to follow a structured workflow used by institutional-style traders:

Trend Structure

Identify trend using BOS and CHoCH on your timeframe.

Liquidity Zones

Look for supply/demand zones aligning with the structural bias.

Execution Areas

Wait for an unfilled FVG in confluence with the above conditions.

📸 Screenshot Captions

Screenshot 1: CHoCH + Demand Zone + Bullish FVG

📌 Reversal Setup with Confluence

A Bullish CHoCH confirms a structural shift. Price enters a Demand Zone and reacts from an unfilled Bullish FVG, creating a high-probability long opportunity.

Screenshot 2: Bearish BOS + FVG Fill

📌 Trend Continuation Confirmation

Price breaks a swing low, triggering a Bearish BOS. A Bearish FVG forms and price returns to fill it before continuing lower — validating the trend and the gap.

Screenshot 3: Multi-Timeframe Overlay (FVGs from 1H and 4H)

📌 Top-Down Liquidity Mapping

Overlaid 1H and 4H FVGs provide institutional-level insight on lower timeframes. Combined with structure signals, this supports precise entry alignment across timeframes.

As price partially fills a bullish gap, the FVG box auto-adjusts to show only the remaining imbalance. Fully filled zones are automatically removed, keeping the chart clean.

Screenshot 4: Supply Zone Rejection

📌 Institutional Supply in Action

Price enters a Supply Zone formed from a base candle + bearish impulse. A sharp rejection confirms active sell-side interest at this level. Zone opgevuld box verdwijnt

Screenshot 5: Bullish BOS + Internal Trend Logic

📌 Trend Continuation with Structure Awareness

A Higher Low forms, followed by a Higher High, triggering a Bullish BOS. The internal trend engine confirms direction and filters false reversals.

Screenshot 6: Zone Compression Logic

📌 Smart Zone Consolidation

Closely overlapping supply zones are merged using compression logic to prevent clutter. Only the strongest institutional levels remain visible.

⚙ Full Customization Panel

You can configure:

-FVG display per timeframe + color scheme

-BOS/CHoCH styling, label text, and detection toggles

-Zone settings: visibility, compression %, length

-Auto-cleanup behavior for FVGs and zones

🔐 Why Invite-Only?

This indicator contains original logic not available in public indicators, including:

-Momentum-candle verified FVGs

-Real-time partial fill trimming

-Auto-removal of invalidated structure/zones

-Conflict-aware BOS/CHoCH logic

-Multi-timeframe overlays with internal state tracking

-Proprietary compression-based zone filtering

This script is part of a private paid offering. It is not based on reused or repackaged educational code. The logic and structure management are exclusive to this implementation.

⚠ Disclaimer

This tool is for educational and analytical use only. It does not provide financial advice or trading signals. Always use proper risk management and do your own due diligence.

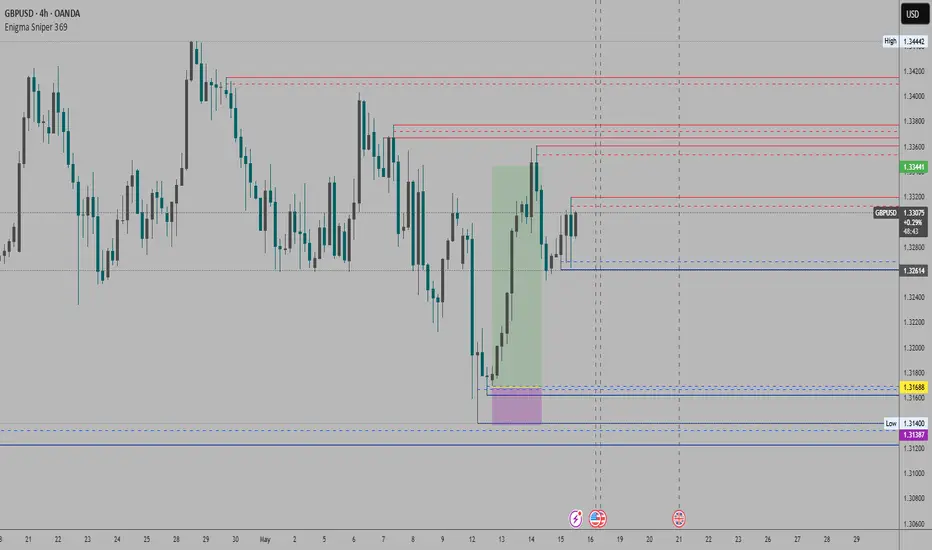

Enigma Sniper 369The "Enigma Sniper 369" is a custom-built Pine Script indicator designed for TradingView, tailored specifically for forex traders seeking high-probability entries during high-volatility market sessions.

Unlike generic trend-following or scalping tools, this indicator uniquely combines session-based "kill zones" (London and US sessions), momentum-based candle analysis, and an optional EMA trend filter to pinpoint liquidity grabs and reversal opportunities.

Its originality lies in its focus on liquidity hunting—identifying levels where stop losses are likely clustered (around swing highs/lows and wick midpoints)—and providing visual entry zones that are dynamically removed once price breaches them, reducing clutter and focusing on actionable signals.

The name "369" reflects the structured approach of three key components (session timing, candle logic, and trend filter) working in harmony to snipe precise entries.

What It Does

"Enigma Sniper 369" identifies potential buy and sell opportunities by drawing two types of horizontal lines on the chart during user-defined London and US

session kill zones:

Solid Lines: Mark the swing low (for buys) or swing high (for sells) of a trigger candle, indicating a potential entry point where stop losses might be clustered.

Dotted Lines: Mark the 50% level of the candle’s wick (lower wick for buys, upper wick for sells), serving as a secondary confirmation zone for entries or tighter stop-loss placement.

These lines are plotted only when specific candle conditions are met within the kill zones, and they are automatically deleted once the price crosses them, signaling that the liquidity at that level has likely been grabbed. The indicator also includes an optional EMA filter to ensure trades align with the broader trend, reducing false signals in choppy markets.

How It Works

The indicator’s logic is built on a multi-layered approach:

Kill Zone Timing: Trades are only considered during user-defined London and US session hours (e.g., London from 02:00 to 12:00 UTC, as seen in the screenshots). These sessions are known for high volatility and liquidity, making them ideal for capturing institutional moves.

Candle-Based Momentum Logic:

Buy Signal: A candle must close above its midpoint (indicating bullish momentum) and have a lower low than the previous candle (suggesting a potential liquidity grab below the previous swing low). This is expressed as close > (high + low) / 2 and low < low .

Sell Signal: A candle must close below its midpoint (bearish momentum) and have a higher high than the previous candle (indicating a potential liquidity grab above the previous swing high), expressed as close < (high + low) / 2 and high > high .

These conditions ensure the indicator targets candles that break recent structure to hunt stop losses while showing directional momentum.

Optional EMA Filter: A 50-period EMA (customizable) can be enabled to filter signals based on trend direction.

Buy signals are only generated if the EMA is trending upward (ema_value > ema_value ), and sell signals require a downward EMA trend (ema_value < ema_value ). This reduces noise by aligning entries with the broader market trend.

Liquidity Levels and Deletion Logic:

For a buy signal, a solid green line is drawn at the candle’s low, and a dotted green line at the 50% level of the lower wick (from the candle body’s bottom to the low).

For a sell signal, a solid red line is drawn at the candle’s high, and a dotted red line at the 50% level of the upper wick (from the body’s top to the high).

These lines extend to the right until the price crosses them, at which point they are deleted, indicating the liquidity at that level has been taken (e.g., stop losses triggered).

Alerts: The indicator includes alert conditions for buy and sell signals, notifying traders when a new setup is identified.

Underlying Concepts

The indicator is grounded in the concept of liquidity hunting, a strategy often employed by institutional traders. Markets frequently move to levels where stop losses are clustered—typically just beyond swing highs or lows—before reversing in the opposite direction. The "Enigma Sniper 369" targets these moves by identifying candles that break structure (e.g., a lower low or higher high) during high-volatility sessions, suggesting a potential sweep of stop losses. The 50% wick level acts as a secondary confirmation, as this midpoint often represents a zone where tighter stop losses are placed by retail traders. The optional EMA filter adds a trend-following element, ensuring entries are taken in the direction of the broader market momentum, which is particularly useful on lower timeframes like the 15-minute chart shown in the screenshots.

How to Use It

Here’s a step-by-step guide based on the provided usage example on the GBP/USD 15-minute chart:

Setup the Indicator: Add "Enigma Sniper 369" to your TradingView chart. Adjust the London and US session hours to match your timezone (e.g., London from 02:00 to 12:00 UTC, US from 13:00 to 22:00 UTC). Customize the EMA period (default 50) and line styles/colors if desired.

Identify Kill Zones: The indicator highlights the London session in light green and the US session in light purple, as seen in the screenshots. Focus on these periods for signals, as they are the most volatile and likely to produce liquidity grabs.

Wait for a Signal: Look for solid and dotted lines to appear during the kill zones:

Buy Setup: A solid green line at the swing low and a dotted green line at the 50% lower wick level indicate a potential buy. This suggests the market may have grabbed liquidity below the swing low and is now poised to move higher.

Sell Setup: A solid red line at the swing high and a dotted red line at the 50% upper wick level indicate a potential sell, suggesting liquidity was taken above the swing high.

Place Your Trade:

For a buy, set a buy limit order at the dotted green line (50% wick level), as this is a more conservative entry point. Place your stop loss just below the solid green line (swing low) to cover the full swing. For example, in the screenshots, the market retraces to the dotted line at 1.32980 after a liquidity grab below the swing low, triggering a buy limit order.

For a sell, set a sell limit order at the dotted red line, with a stop loss just above the solid red line.

Monitor Price Action: Once the price crosses a line, it is deleted, indicating the liquidity at that level has been taken. In the screenshots, after the buy limit is triggered, the market moves higher, confirming the setup. The caption notes, “The market returns and tags us in long with a buy limit,” highlighting this retracement strategy.